Data reveals that “[i]n 2023, Florida car insurance rates increased year over year at almost double the rate of the national average.”

Our anecdotal experience affirms this; hardly a week goes by that we don’t hear someone complain about how much her auto insurance rates have gone up. For those who keep abreast of current events, including the passage in March of major “tort reform” in Florida, there is hope that relief is in sight.

Unfortunately, despite the significant shifts in Florida’s legal terrain, it’s unlikely that many Floridians will see much, if any savings in their auto insurance premiums any time soon.

The role of underwriting

A big reason is because insurance premiums are tied to the underwriting process. Underwriting is the process insurance companies undertake to assess risk (i.e., the likelihood that an insurance claim will eventuate). To do that in the auto insurance realm, a number of variables are considered.

Some of the factors make sense and ostensibly, are things consumers can/should consider:

- Coverage: Plainly, the more coverage carried, the higher the premium. An easy way to cut costs is to reduce coverage limits (as to the optional types of coverage, such as liability coverage); or increase deductibles on coverages that allow for that (such as collision and comprehensive); or even drop coverage (for example, dropping comp and collision on an older vehicle).

- For those folks with assets, good insurance serves as an important asset protection tool; and

- Everyone should be aware that about 1 in 4 drivers on Florida roads is uninsured, which makes uninsured motorist coverage a worthwhile investment in protecting you and your loved ones should they get in an accident.

- Vehicle (make and model): Owning a luxury SUV or a high-performance sports car has lots of perks! Because, however, such vehicles are pricier than most and have more expensive parts than a budget-friendly, practical sedan, they are more expensive to insure.

- Mileage: Drive less, pay less. Recall that much to the surprise of many, some insurance companies actually refunded policyholders a portion of their premiums in the early days of the pandemic. The simple reason for that ‘generosity’ was largely about the fact that people were at home, working from home, and generally not venturing out much. In turn, fewer chances for a fender-bender leading to an insurance claim arose.

- Ownership status of car: Obviously leasing or financing a car creates a monthly car payment. Often, there are unrecognized, additional costs associated with this arrangement that someone who owns his car outright might choose not to pay for. Specifically, in addition to the mandatory minimum Florida insurance coverages (of No-Fault/PIP insurance and Property Damage coverage), typically the leasing company or bank is going to also require liability coverage, comprehensive and collision coverage, among other coverages. While not necessarily prudent, an outright owner can choose not to carry such coverages.

Before making dropping coverage, however, be mindful that

Other less controllable variables

Other considerations are a matter of demographics, which we don’t have much control over:

- Age: To no one’s surprise, teens, known for impulsive and often pretty lousy decision-making, do that behind the wheel too. Consequently, as a group, they pay higher premiums than other age groups (though teens who are good students may earn a reprieve in the rates being charged). Thankfully, by age 25, rates ease and continue along that trajectory … until they start to rise again. Older drivers, with issues like slower reaction times, are once again a riskier group to insure and so pay more (though again, some insurance companies offer discounts for those who take safe driving courses or the like).

- Gender: As is well-known to every parent of a teenage driver, teenage boys cost more to insure than teenage girls. Fortunately, the gender factor wanes as those teenage boys mature.

- Marital Status: Believe it or not, single, divorced, and widowed people pay more for insurance than married folks. Data apparently backs up this distinction. Fortunately, the difference is not a lot (i.e., saving on insurance is not a good reason alone to rush to the altar).

Some parts of your past might contribute, too

Past is prologue. That is, there’s not much that can be done to change what’s already occurred.

- Driving Experience: Put simply, practice pays. The more experienced driver trumps the neophyte driver. Some mitigating steps, such as completing a driver training program or getting good grades, can help make up for the lack of experience.

- Driving Record: Those with a history of insurance claims, traffic citations, accidents, DUIs, etc. not surprisingly face higher premiums.

- Credit History: More surprising, is that people with poor credit typically pay more for insurance. That’s because data shows that those with credit issues also tend to file more and more costly claims than those with good credit.

- Insurance History: Failing to consistently carry insurance is another red flag … of possible uninsured driving in the past. And that red flag can lead to being charged a higher premium.

As between insurance companies, premiums charged for similar coverage can vary, sometimes a lot. The reasons are undoubtedly many, but likely reflect that some of these factors carry more or less weight from company to company. Given this, it’s worth shopping around!

Along the way find out if there are programs or discounts that allow for more savings. Options abound. Good students, completing a driver safety course, the military, government employees, loyal customers, customers who bundle other insurances, and even customers who agree to have a tracking device placed on their car are often eligible for favored status.

The likely impact of Florida’s 2023 Tort Reform

Florida’s highly-lauded (by some) 2023 Tort Reform legislation does not address let alone mention, anything about lowering insurance premiums.

Instead, there is lots of oblique talk about how these reforms cost Floridians…leaving many to reasonably assume that they will in turn save money on their premiums. The bottom line is that that is unlikely.

A closer look at the “cost” is enlightening. By cost, we are referring to what proponents of tort reform frequently cited when talking about the need for these new laws. Namely, that Florida families bear a $5065 burden which this legislation will [somehow] address.

First, the origin of that $5065 figure. That number derives from a study by the US Chamber of Commerce and honestly requires a deep dive into the weeds to better understand how the figure was computed.

The figure comes from a simple calculation: the total claims dollars paid out in Florida in 2020 ($40,173M) divided by the number of Florida households (7,931,313).

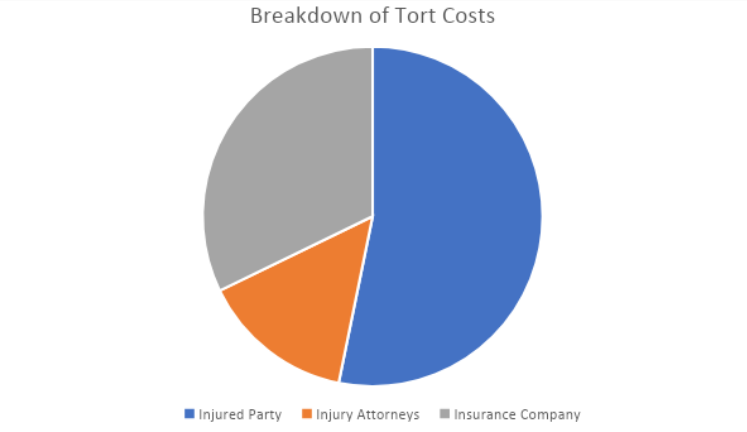

Next, understanding what the total claims dollar figure (i.e., the $40,173M) accounts for or includes is enlightening. This is where opacity comes into play because, as they say, the devil is in the details (i.e., don’t overlook the end notes, especially 23). As it turns out, the gross dollars paid out figure allows for not just what the injured party receives (namely 53.2% of every dollar), but also allows a portion (specifically, the remaining 46.8%) that the involved attorneys and insurance companies get (or keep) to cover the risks they assume,* their respective costs of doing business and their profits.** That revealingly shows that of the dollars paid out, the injury attorneys take 14.6% while the insurance companies, including their in-house and outside claims handlers and attorneys, take/keep 32.2%.

To our mind, facts like this undercut a lot of what was said by proponents of tort reform, who lay the blame for at the feet of the plaintiff’s injury attorneys.***

* In the risk department, plainly, insurance companies are in the business of insuring risk and (as the aforementioned discussion makes clear) assessing premiums accordingly. Injury attorneys, who typically work on a contingency fee basis (i.e., no fees or costs unless we win) assume risk too – they earn $0 if a case is lost (which in turn means that most are not going to prosecute a frivolous claim).

** The cost of doing business covers pretty much everything from hiring and paying employees to having the equipment and space etc. they need to do the work of the business, so that ultimately the business’ revenues exceed the expenses and profit is earned.

*** A soundbite from a lobbyist for State Farm (whose CEO has recently reportedly earned over $20M in recent years), characterized Florida’s auto insurance rates as “frankly a tax by the rich plaintiffs’ bar against the poor working families of Florida.” Similarly, the head of Florida’s Chamber of Commerce blamed “personal injury billboard trial lawyers” as being responsible for “billions of dollars spent annually on frivolous litigation”.

In the end, the tort reform legislation’s primary will reduce what insurance companies have to pay on claims.

Among other changes, medical bills incurred by an injured person can now be attacked as unreasonable.

And it gives insurance companies much more freedom and room to do what they do: delay, defend, and drag out the process. Call us cynical, but betting that Florida families will see much of that $5,065 cost savings seems unlikely. Your best bet? Keep price shopping for the best rates possible.